Creating a monthly budget isn’t about restricting your life—it’s about taking control of your money, reducing stress, and making sure your income works for you, not the other way around. A budget that “actually works” is realistic, flexible, and easy to follow.

Below is a step-by-step guide to building a monthly budget you can stick to.

Why Most Budgets Fail

Before creating a budget, it’s important to understand why many don’t work:

- They are too strict or unrealistic

- People forget irregular or hidden expenses

- No room is left for fun or personal spending

- Tracking is inconsistent

- Goals are unclear

A successful budget fixes these problems from the start.

Step 1: Calculate Your Total Monthly Income

Start with your actual take-home income, not your gross salary.

Include:

- Salary after taxes

- Freelance or side income

- Rental income

- Passive income (interest, dividends)

Tip: Use an average if your income changes month to month.

Step 2: Track Your Monthly Expenses

Track at least 30 days of spending to see where your money really goes.

Fixed Expenses (Mostly the Same Every Month)

- Rent or mortgage

- Utilities

- Insurance

- Internet and phone bills

- EMIs or loan payments

Variable Expenses (Change Monthly)

- Groceries

- Dining out

- Transportation

- Entertainment

- Shopping

Irregular Expenses (Often Forgotten)

- Medical bills

- Annual subscriptions

- Repairs and maintenance

- Gifts and festivals

- Travel

Tracking tools, bank statements, or budgeting apps can help here.

Step 3: Categorize Your Spending

Divide your expenses into clear categories such as:

- Housing

- Food

- Transportation

- Savings

- Debt

- Personal & lifestyle

- Entertainment

This helps identify overspending areas quickly.

Step 4: Choose a Budgeting Method

Pick a system that fits your lifestyle.

1. 50/30/20 Rule

- 50% Needs (rent, food, bills)

- 30% Wants (shopping, entertainment)

- 20% Savings & debt repayment

Best for beginners.

2. Zero-Based Budget

Every rupee/dollar has a job.

Income – Expenses = 0

Best for people who want full control.

3. Envelope Method

Cash or digital envelopes for each category.

When the envelope is empty, spending stops.

Best for overspenders.

Step 5: Set Realistic Financial Goals

Budgets work better when tied to goals.

Short-Term Goals

- Emergency fund

- Paying off credit cards

- Saving for a phone or gadget

Long-Term Goals

- Buying a house

- Retirement

- Children’s education

Clear goals create motivation to follow your budget.

Step 6: Pay Yourself First

Before spending on anything else:

- Transfer money to savings

- Invest a fixed amount

- Fund your emergency account

Treat savings like a non-negotiable bill.

Step 7: Plan for Fun and Flexibility

A budget that doesn’t allow enjoyment will fail.

- Set a guilt-free spending amount

- Allow flexibility for unexpected expenses

- Adjust categories as life changes

A working budget is flexible, not perfect.

Step 8: Review and Adjust Monthly

At the end of each month:

- Review spending vs budget

- Identify problem areas

- Adjust categories if needed

Your first budget won’t be perfect—and that’s okay.

Common Budgeting Mistakes to Avoid

- Ignoring small daily expenses

- Forgetting annual or seasonal costs

- Being too strict

- Not tracking regularly

- Giving up after one bad month

Consistency matters more than perfection.

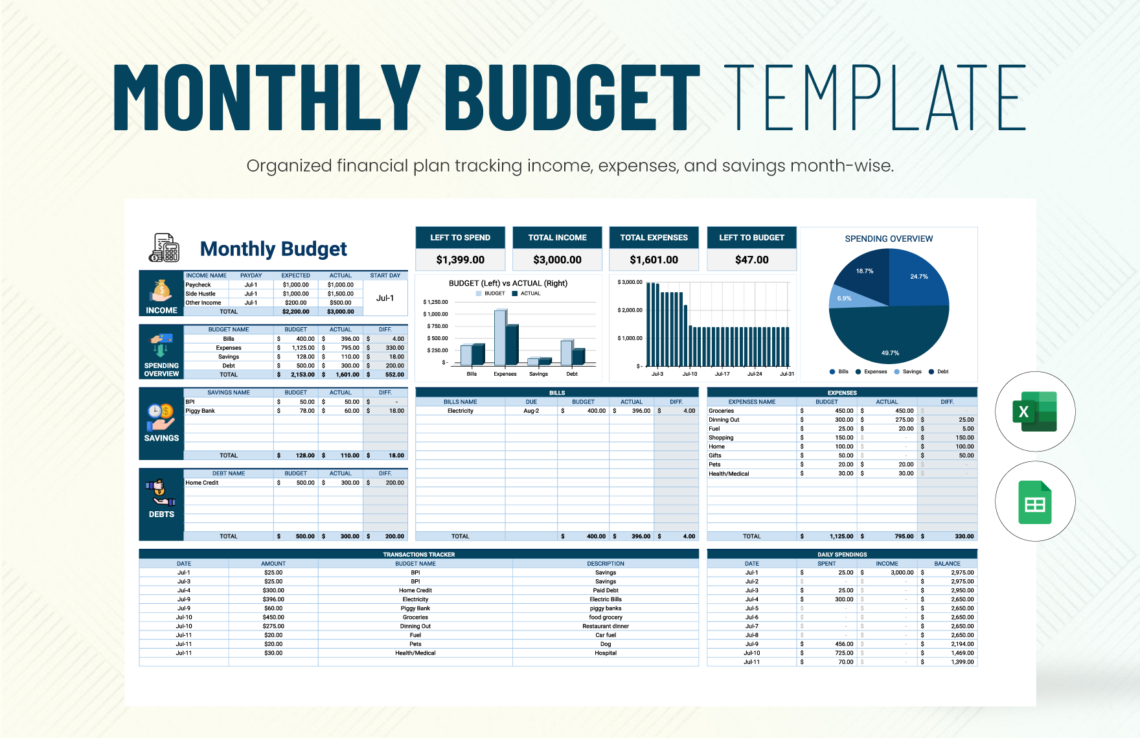

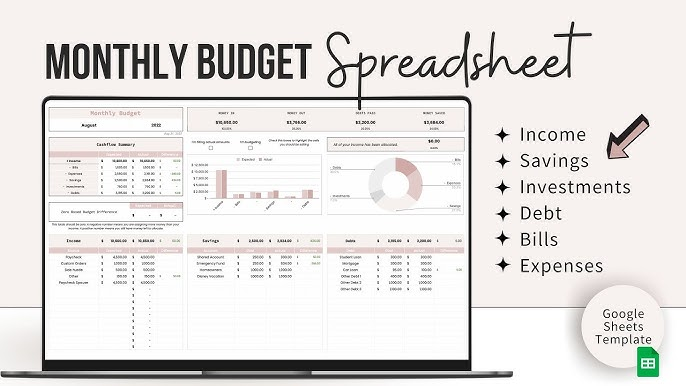

Tools That Can Help

- Budgeting apps

- Excel or Google Sheets

- Bank expense trackers

- Manual notebooks

Use whatever you’ll actually stick with.

Final Thoughts

A monthly budget that actually works is:

- Simple

- Realistic

- Flexible

- Goal-oriented

Once you control your budget, you control your future. Start small, stay consistent, and adjust as you grow.

#MonthlyBudget #PersonalFinance #MoneyManagement #BudgetingTips #FinancialPlanning #SavingsGoals #SmartMoney #FinanceBasics #DebtFreeJourney #Anslation #Carrerbook